Financial Equity for the Unbanked: Challenges and Solutions

July 09, 2024 by Lisa Moore

The evolution of technology has drastically transformed the payments landscape, particularly in the realm of money disbursements. While many enjoy the convenience, simplicity, and security of modern banking, a surprising number of U.S. residents remain unbanked, relying solely on cash.

For these individuals, receiving money digitally or by check presents significant challenges. This lack of access to banking services puts them at a considerable disadvantage, exposing them to exorbitant check-cashing fees, cash-only payment hassles, delays in receiving funds, financial exclusion, and potential loss or theft associated with carrying large sums of cash.

This blog is Part 1 of a two-part series on financial equity for the unbanked.

What Does It Mean to Be Unbanked?

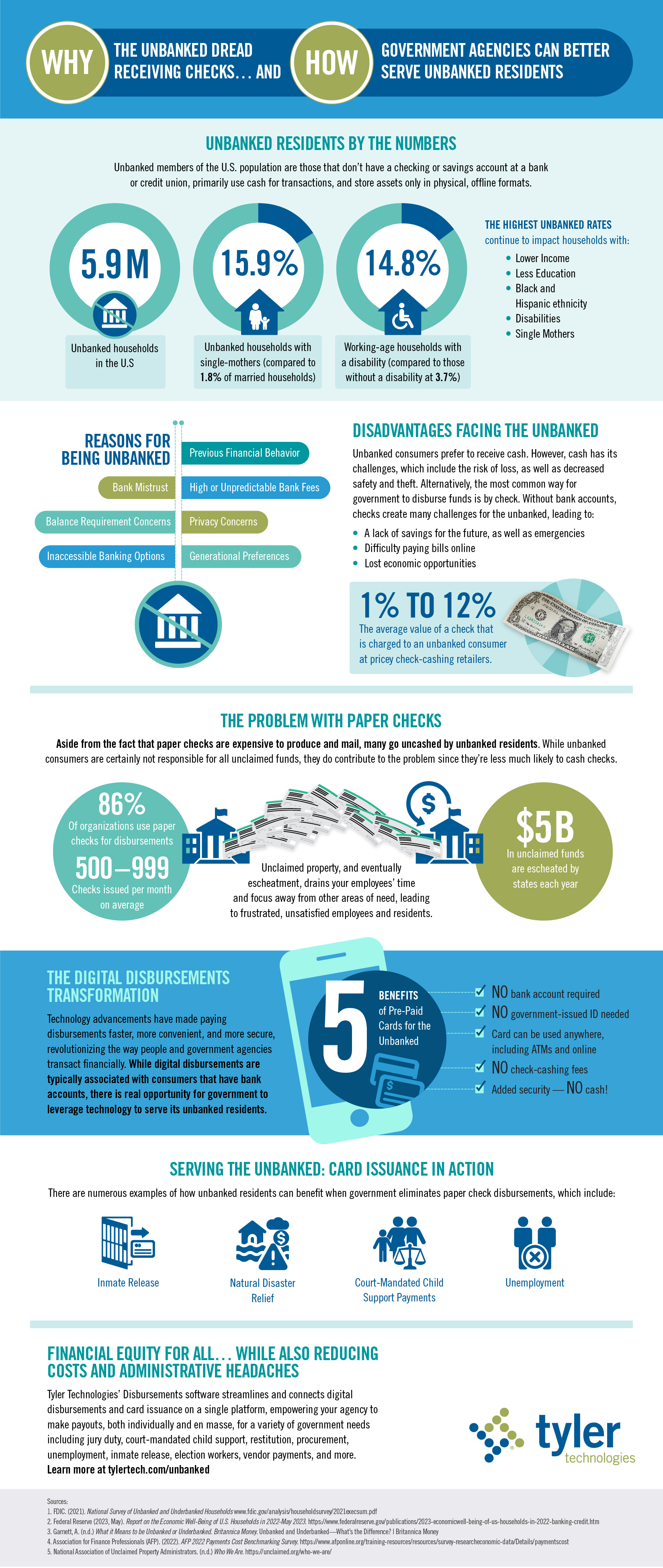

Unbanked individuals in the U.S. do not have checking or savings accounts at banks or credit unions. They primarily use cash for transactions and store assets only in physical, offline formats.

According to the most recent FDIC report in 2021, there were 5.9 million unbanked households in the United States. The percentage of unbanked individuals was also higher among Black, Hispanic, low-income, less-educated, and single-mother households. For instance, while households with married couples made up only 1.8% of the unbanked population, single-mother households accounted for a staggering 15.9%. Additionally, southern states had the highest unbanked rates, with 4.9% of the population being unbanked.

Why Are People Unbanked?

Several factors contribute to individuals being unbanked:

- Previous financial behavior: Past financial mismanagement or lack of experience with formal banking can deter people from opening bank accounts.

- Bank mistrust: Some individuals do not trust banks due to negative experiences or perceived lack of transparency.

- Balance requirement concerns: Many banks require minimum balances, which can be a barrier for low-income individuals.

- Privacy concerns: Concerns about data security and privacy can deter people from using banks.

- High or unpredictable bank fees: Fees associated with maintaining bank accounts can be a significant barrier for the unbanked.

- Inaccessible banking options: In some areas, especially rural or underserved communities, access to banking services is limited.

- Generational preferences: Some people may prefer cash-based transactions due to cultural or generational habits.

Disadvantages Facing Unbanked Consumers

Receiving money in cash presents numerous disadvantages. Shamina Singh, president of the Mastercard® Center for Inclusive Growth, highlights the broader impact: "Cash is not a friend of the poor. Think about 2 billion people around the world who are trapped in an economy where they can only transact with people they know and see, in a very small geography."

She further explains, "[The unbanked] are excluded from the financial systems that allow for economic mobility."

The most common way for government agencies to disburse funds is by check. Without bank accounts, checks create many challenges for the unbanked, including:

- Lack of savings for emergencies: Without bank accounts, it's difficult for individuals to save money securely, leaving them vulnerable in emergencies.

- Difficulty paying bills on time: Managing bills can be challenging without access to online banking or direct debits.

- High check-cashing costs: Unbanked individuals often rely on check-cashing services that charge high fees, typically 1-12% of the value of the check.

- Delays in receiving funds: Mailing checks can delay access to necessary funds.

- Lost economic opportunities: Lack of access to banking services can hinder economic mobility and opportunities for financial growth.

What Solutions Are Available for the Unbanked?

Addressing financial inequity for the unbanked requires a multifaceted approach. Government agencies have a duty to promote financial equity for this underserved population. Modern disbursements technology, coupled with prepaid cards, are changing the way government agencies serve unbanked residents for things like court-mandated child support payments, unemployment benefits, inmate release payments, and natural disaster relief.

5 Benefits of Prepaid Cards for the Unbanked

- No bank account required

- No government-issued ID needed

- The card can be used anywhere, including ATMs and online.

- No check-cashing fees

- Added security — no carrying large amounts of cash!

The Time Is Now

By eliminating check-based disbursements to residents, government can become more financially inclusive, better serve unbanked residents, and help provide families with more economic opportunities.

Modern disbursements technology like Tyler’s Disbursements and Card Issuance software offers a promising path toward financial equity, ensuring that all individuals have the tools they need to participate fully in the economy. In Part 2 of this series, we’ll explore the other side of the story — challenges faced by government agencies — and the positive impact digital disbursements have had inside the halls of government.